The “SOCIAL SECURITY ELEPHANT” in the Room

June 12, 2025By Michael Owens, CFF, CRPS

Carolina Financial Services Group

When, Why and How Should I File for Social Security to Balance my Benefits, Tax Exposure, and Retirement Lifestyle?

Nearly 90% of Social Security claimants fail to make the optimal claiming decision. That means they lose out on an estimated $3.4 trillion in potential retirement income (on average $111,000 per household). The average recipient would receive 9% more income in retirement if they made the financially optimal decision about when to claim this retirement benefit.1

Even the Social Security Administration has acknowledged that it has sometimes given out incorrect information. In fact, poor advice from the Social Security Administration itself has cost widows and widowers an estimated $130,000 million in benefits.2

There’s no such thing as a boilerplate Social Security strategy. There are over 2,700 rules and hundreds of filing combinations to consider when deciding to claim your Social Security benefits.3

WHEN SHOULD YOU CLAIM SOCIAL SECURITY?

The #1 question that’s on most people’s minds as they approach retirement is, when should they claim Social Security? You’ll be eligible to claim 100% of your Social Security benefit at your Full Retirement Age, but you’re allowed to claim Social Security as early as age 62. Depending on when you were born, your Full Retirement Age is between age 66 and 67.

Key Consideration: The earlier you file, the less you’ll receive in benefits each month – for as long as you continue claiming.

Claiming Social Security EARLY (Between ages 62-67)

While claiming Social Security early reduces your monthly benefit, it also means that you’ll be collecting checks longer. Delaying benefits by one year could increase the size of your benefit by 5% to 8%, depending on your age at the time.4

Here are a few common reasons why you might want to claim Social Security early:

- You need income early in retirement

- You don’t want to draw down your retirement savings yet (and want to let them grow at market rates)

- You have a high-earning spouse, and want to let their benefit potentially grow while claiming your own

- You believe you might have a lower life expectancy than average

Claiming Social Security at YOUR FULL RETIREMENT AGE (Age 66-67)

If you claim at your Full Retirement Age (FRA), you’ll get 100% of your full benefit, but you’ll give up the opportunity to let your benefit continue to grow.

There are 3 primary reasons to claim at your FRA:

- You won’t lose out on any benefit amount

- You can work and still collect your full benefit (because the Annual Earnings Limitation goes away)

- You can suspend your benefits at any time to allow them to start growing again

***If you were born before January 2, 1954, you may still be eligible to file a “Restricted Application” to maximize your lifetime benefits.5 This advanced strategy is a powerful tool for married couples who want to potentially maximize their income, protect a surviving spouse, and manage tax consequences.

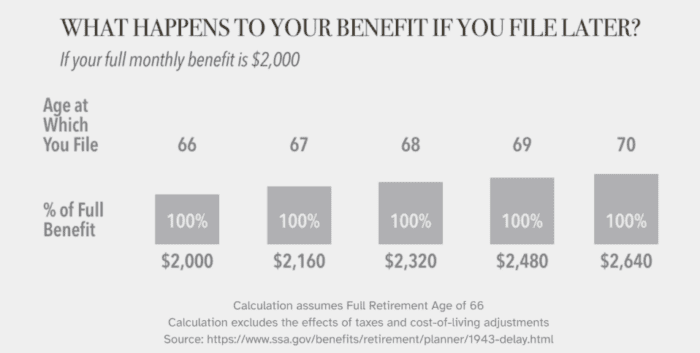

Claiming Social Security at AGE 70

If you delay claiming Social Security past your Full Retirement Age, your benefit will grow each year until you reach age 70. Since your benefit doesn’t grow past age 70, there’s no reason to delay claiming past that age.

Choosing the Wrong Social Security Path Could Cost You Thousands of Dollars Per Year of Lost Income

While claiming your Social Security benefits is as simple as filing an application on the Social Security Administration’s website, it’s not a decision to take lightly. Before you claim, I strongly urge you to take the following steps:

Step 1: Consider all the options available to you and your spouse

Step 2: Talk to a professional about your retirement income strategy

Step 3: If you think you’ve made a mistake in filing (or you think you’re better off with a different strategy), call my office immediately. We may be able to help you “turn back the clock” on your benefits so you can potentially optimize your income.

Here’s what getting a professional opinion on your Social Security strategy and retirement income plan can deliver:

- Software that analyzes Social Security rules and shows you how to optimally claim Social Security designed to maximize income now and later

- A personalized analysis of advanced claiming strategies, including 62/70, Start-Stop-Start, Claim and Grow, and limited-opportunity strategies

- A tax savvy income strategy that shows you ways to structure withdrawals from retirement accounts and Social Security to help minimize taxes

If you’ve already started claiming Social Security, it may not be too late to get advice and make a change. If we find you’re better off with a different claiming strategy, we can help you “turn back the clock” with the SSA and get back on the right track.

Stay Flexible. Stay Informed.

If you have questions about how this outlook affects your retirement journey, I’d love to talk.

📞 (252) 215-9095

📧 mowens@cfsgroup-nc.com

Sources

- https://www.usatoday.com/story/money/2024/07/07/best-time-collect-social-security-retirement-benefits/74315804007/

- https://www.forbes.com/sites/johngoodman/2024/03/11/how-to-reform-social-security-part-1/

- https://www.goodmaninstitute.org/2023/02/27/social-securitys-massive-malfeasance-2/

- https://www.fool.com/retirement/social-security/how-much-social-security-increase-after-62/